How do you develop persistence and resilience to improve your organisational performance? How can you use grit to enhance your leadership skills? What does grit even mean?

Seize the opportunity to elevate your success in the workplace and achieve inspiring leadership with PEMANDU Associates’ Learning Academy Masterclass, Beyond Grit: Achieving High Performance. This one-day programme welcomes individuals wanting to achieve quantum improvement in their performance as well as heads of departments and managers in charge of affecting change and transformation (Programme Management Office, Transformation Management Office and Strategy Office).

Date: Wednesday, 14 November 2018

Time: 9.00 am – 5.30 pm

Location: Meet on 35 @ Sunway Putra Hotel

Fee: RM990 per person (HRDF claimable)

This workshop will cover:

Module 1: Connecting to Your Passion and Empowering Them

Module 2: Cultivating Grit

Module 3: Developing a Growth Mindset to Achieve Success

Module 4: The Different Success Factors Associated with Effective Performance

Module 5: Building a Circle of Success

Seats are limited. Register by Friday, 9 November 2018 to secure your seat!

Business tourism is defined by the International Congress and Convention Association (ICCA) as “the provision of facilities and services to the millions of delegates who annually attend meetings, congresses, exhibitions, business events, incentive travel and corporate hospitality”.

It is an expansion of the traditional Meetings, Incentives, Conferences and Exhibitions (MICE) sector by interconnecting with activities within the tourism sector of the host country. Attracting business tourists to attend events at a host country is crucial as over 25% of international delegates are likely to bring their spouses along with approximately 65% of these delegates returning with family and friends in the future (Economic Transformation Programme [ETP] Lab Report, 2010).

Business tourism itself had a larger multiplier effect to the economy. Furthermore, it was less affected by seasonal price fluctuations and was typically used to reduce the ‘peak-trough’ differences in the year.

However, Malaysia was trailing behind Singapore, Indonesia and Thailand in the business tourism sector as events in Malaysia were mainly fuelled by small to mid-sized local and regional conference events. This presented a strong case for Malaysia to develop and be positioned as a leading business tourism destination to attract high-quality international events with large numbers of delegates. This, in turn, was targeted at translating into higher receipts quantitatively as well as generate qualitative benefits in terms of enhanced trade and know-how. It was estimated that for every RM1 spent by the government of Malaysia, there was a return-on-investment of RM111 in revenue obtained by the business tourism industry (ETP Lab Report, 2010).

The Malaysian Convention & Exhibition Bureau (MyCEB) that was set up in 2009 was specifically formed to drive the growth of the business tourism ecosystem in Malaysia. To help formalise its operations and funding from 2010 onwards, business tourism became one of the Entry Point Projects (EPP) under the Tourism National Key Economic Area (NKEA), one of the sectors identified under the National Transformation Programme. The Tourism NKEA had an ambitious goal of growing the business tourism sector to reach an 8% share of total tourist and international delegate arrivals by 2020 from a baseline of 5% in 2009.

Detailed Action Steps and Solutions Undertaken

Three main approaches were taken by the government to develop the sector:

Strengthening core operations to drive the industry

Provision of adequate funding to develop the sector

The Performance Management and Delivery Unit (PEMANDU, now a private entity known as PEMANDU Associates), then part of the Prime Minister’s Department of Malaysia, played a pivotal role in securing adequate funding from the government for MyCEB’s operations and development of the industry. The subvention funds issued by MyCEB to the private sector were allocated via a stringent mechanism and careful monitoring to ensure these funds were utilised to support achievement of the number of tourist arrivals and yield.

Implementation of a robust monitoring mechanism

This EPP’s progress was tracked via a stringent monitoring mechanism put in place by PEMANDU. Robust Key Performance Indicators (KPI) were crafted to drive achievement of the desired outcomes for this project. The indicators measured were primarily focused on the number of international delegates secured for each event and the estimated economic impact from the events hosted. The progress in achieving the KPIs were reported monthly while implementation issues were reviewed and resolved on a weekly basis.

Change of event management to maximise tourist yield

Taking a step further from event organisation, additional activities were conducted by MyCEB to tie the business events with other tourism activities. Cross-selling opportunities were taken where each event was provided pre and post-event tour options and delegates were clearly informed of the tourist activities available in order to maximise yield.

Coordination of players

Leveraging on industry experts

Getting the private sector to take ownership in developing the industry together was crucial. Thus, the Malaysia Conference Ambassador ‘Kesatria’ Programme made up of key opinion leaders and industry experts was launched in 2012. The programme’s objective was to encourage potential local hosts to bid for and stage international conventions. 47 ‘Kesatria’ ambassadors have been appointed, generating 135 leads with the potential to bring in 200,000 delegates and an estimated economic impact of RM2.1 billion.

Improving government’s facilitation of the industry

In addition to the focused attention by MyCEB, the government played a strong role in facilitating the growth of the industry. A Steering Committee comprising representatives from then-Ministry of Tourism and Culture (MOTAC), Ministry of Finance, Ministry of Home Affairs, Ministry of International Trade and Industry, MyCEB, events-related associations and other relevant private sector stakeholders met monthly to review and problem-solve implementation issues on business tourism related activities. Notable issues resolved included immigration requirements for exhibition delegates and international speakers to improve Malaysia’s attractiveness. An inter-ministerial committee with representatives from all ministries was also set up in 2016 to coordinate the involvement of the government for the events to be hosted in Malaysia and minimise overlap of resources provided.

Providing an enabling environment

Capacity-building of the industry

In order to support the development of professional standards and skills training for event organisers, the Industry Partner Programme was established under MyCEB in 2011. This programme’s objectives were to provide access to market insights, encourage industry training and certification as well as facilitate co-operative marketing and promotions efforts. This activity was instrumental in ensuring a pipeline of capable event organisers who will be able to continue spearheading the industry.

Development of shell sites

Shell sites are required to host events such as gala dinners. Iconic shell sites can differentiate Malaysia from its competitors in other countries and provide a draw for organisers to host their events here. In Malaysia, no dedicated site existed as at 2010. Under this initiative, four shell sites were formally recognised comprising Central Market, Thean Hou Temple, Forest Research Institute of Malaysia (FRIM) and Maritime Centre Putrajaya.

Impact and Results

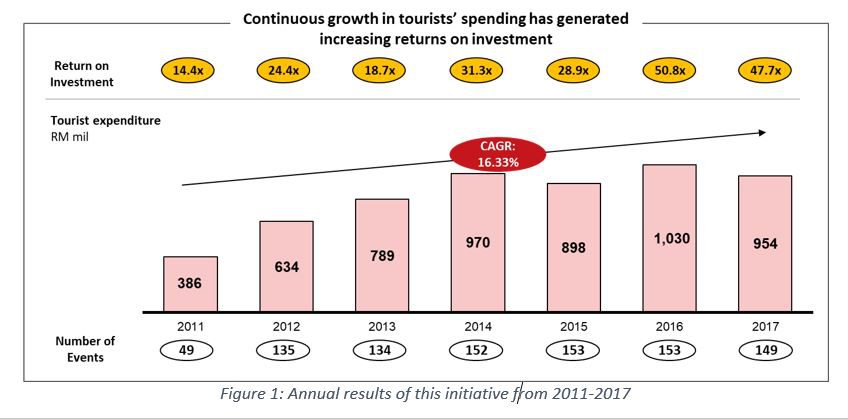

As a result of the concerted efforts spearheaded by MyCEB and supported by key stakeholders, business tourist expenditure grew at a CAGR of 16.3% from RM386 million since the launch of project in 2011 to RM954 million in 2017. The number of events secured annually also grew from only 49 in 2011 to reach 149 in 2017 with significant return of investment growth from 14.4 times in 2011 to a high of 47.7 times in 2017 (MyCEB, 2017).

In total, this EPP supported 2,013 events between 2010-2017 and attracted more than 943,146 international delegates to Malaysia, which translated to an estimated RM11.5 billion in economic impact to Malaysia. The share total arrivals from business tourism grew from 5% in 2009 to 7% in 2017 (ICCA, 2017).

Malaysia successfully secured and hosted various prestigious international events as exemplified below (list is non-exhaustive):

No

Year

Notable events

1

2011

The Institute of Internal Auditors (IIA) International Conference

2

2012

25th World Gas Conference

3

2013

Seventh International AIDS Society (IAS) HIV Conference in Pathogenesis, Treatment and Prevention 2013

4

2014

15th International Architecture, Interior Design & Building Exhibition (ARCHIDEX)

25th International Invention, Innovation and Technology Exhibition (ITEX 2014)

5

2015

127th International Olympic Committee (IOC) Session

6

2016

Institute of Electrical and Electronic Engineers’ International Conference on Communications 2016 (IEEE ICC)

55th International Congress and Convention Association (ICCA) Congress

7

2017

The International Federation of Freight Forwarders Associations (FIATA) World Congress

General Assembly of the International Co-operative Alliance (ICA) 2017

8

2018

World Urban Forum 2018

Hosting these international events increased Malaysia’s global recognition as a leading business tourism destination. In addition, this positively impacted various ancillary components such as accommodation, catering, logistics, events management as well as increasing the spillover effect for leisure tourism. In 2016, Malaysia was ranked 10th for business travel contribution in the World Travel and Tourism Council (WTTC)’s ranking. WTTC also reported that an analysis from Oxford Economics had shown that business travel spending in Malaysia was significantly higher than leisure travel and the average in the ASEAN region (WTTC, 2016).

As there was no dedicated body or initiative overseeing the development of this sector previously, the growth can be attributed to the success of this EPP under the Tourism NKEA.

Lessons Learnt and Recommendations

A key lesson learnt from this initiative is that it is highly imperative to have a dedicated body to spearhead the development of this sector and coordinate the various players from both the public and private sectors. Without a dedicated body to push the business tourism agenda forward, the initiative would not have been able to grow as rapidly. In addition, adequate funding support was critical to ensure continuous development as any reduction would directly impact the amount of subvention funds that could be provided, thus reducing the number and size of events that could be secured.

The involvement of private sector associations was also important to bridge the last mile in securing international organisers as well as provide the relevant expertise to ensure the success of the events. For example, the Malaysian Association of Convention and Exhibition Organisers and Suppliers (MACEOS) contributes to the development of this industry with its network and understanding of the industry, including the operations and execution of hosting international events. MyCEB plays a role to assist the association in market intelligence, bidding package and proposals to secure Malaysia as the host destination.

Another lesson learnt was that it was crucial to secure the support of other ministries and agencies. This is important as the involvement of the relevant ministry in charge, with the attendance of senior civil servants or the minister, serves as a draw for international event organisers. One of the ways to address this during the implementation phase was to create an inter-ministry coordination committee to coordinate the planning, securing, and organising of the business events hosted in Malaysia. This proved an important step in ensuring wider reach of MyCEB from only being under the purview Ministry of Tourism & Culture, to also work with various ministries which oversee policies such as industry development, the economy, immigration and trade.

Moving forward, PEMANDU Associates continues to have the view that a strong dedicated body to drive this sector is necessary, equipped with adequate funding and emphasising on recognised ROI, to support the growth of this industry. In addition, strong coordination and cooperation between the public and the private sectors is crucial to ensure the success of this industry.

Increasing production. Rising inventory. Slumping prices. If recent developments in the palm oil sector are indicative of its future, the sector certainly looks bleak. Or does it?

Global population is set to grow from the current 7.6 billion to 9.8 billion in 2050[1], with 70% living in urban areas[2]. The middle-income class continues to boom. By 2027, this segment is expected to reach 5 billion, representing 60 % of the global population[3].

This growth will be accompanied by an ageing population as the number of people aged 60 or above is expected to more than double by 2050, rising from 962 million globally in 2017 to 2.1 billion in 2050[4]. Life expectancy is rising, from 65 years for men and 69 years for women in 2000-2005 to 69 years for men and 73 years for women in 2010-2015[5], with further improvements expected moving forward.

These demographic changes point to greater demand for food, feed, fuel as well as consumer and health products, all of which can be fulfilled by vegetable oils, including palm oil. Maybe, things are not so bleak after all, but let’s examine the facts.

Feeding the growing world

To meet growing demand, the world will inevitably see an expansion of land use for oil crops such as palm oil, soy, rapeseed, sunflower, coconut and others.

Palm oil is superior to other oil crops in respect of yield productivity. On average, oil palm yields about 3.5 tonnes from a hectare of land. Other oil crops such as rapeseed oil, sunflower seed oil, soya bean oil and coconut oil can only yield 0.8 tonnes/ha, 0.7 tonnes/ha, 0.4 tonnes/ha and 0.3 tonnes/ha respectively.[6] Hence, palm oil requires significantly less land to produce the same quantity of oil.

Yet, palm oil cultivation is facing immense pressure from environmentalists. In 2017, the European Parliament passed a resolution to ban palm biofuel from 2021 and to impose a single certification scheme for all palm oil entering the European Union, citing concerns on deforestation. Following tremendous protest by producers such as Indonesia and Malaysia, this stance was later softened to only exclude palm biofuel along with all other vegetable oil-based biofuel in 2030.

Disproving critics

But is there basis for the allegations on deforestation? Statistics suggest not. In fact, livestock rearing is the main culprit while soy cultivation causes forest loss at almost double the rate for oil palm cultivation.

Moving forward, we will witness a combination of oil crops delivering environmentally optimal vegetable oil supply. Banning palm oil expansion may in fact worsen the environmental impact. A cost and benefit analysis for palm oil expansion conducted in 2013 by James Fry, a leading palm oil expert, showed startling results. Had a moratorium been imposed on oil palm cultivation in 2013, the world would have lost an incremental 145 million hectares of forest to make up for that loss of production. This stems from the need to expand other crops at a faster rate to close the supply gap from palm oil.

Given the worldwide population growth trend and the need to feed the population, there is no doubt that palm oil must and will remain in the mix. The more pertinent question is how palm oil planting can be expanded sustainably.

Co-existing with the natural environment

Sustainability must be the utmost priority in palm oil business. To co-exist symbiotically with the environment, the industry must prioritise a balance between economic development and environmental sustainability, avoid deforestation and optimise land use, protect biodiversity and adopt robust standards.

Teresa Kok, Minister for Primary Industries of Malaysia recently reiterated the policy of capping palm oil expansion to ensure 50% forest cover.[7] Such bold policy actions should be lauded as it signals commitment by the government to reduce deforestation and protect biodiversity in one stroke of policy.

Adopting sustainability standards is the most practical and impactful approach that can be taken by palm oil stakeholders. To date, the globally recognised Roundtable for Sustainable Palm Oil (RSPO) has certified total of 19% of palm oil produced across the globe. In complementary moves, Indonesia and Malaysia have both enacted their own national standards, namely Indonesian Sustainable Palm Oil (ISPO) and Malaysian Sustainable Palm Oil (MSPO). However, both certification schemes have yet to gain extensive acceptance, by both governments and private sector buyers.

The execution of sustainability policies must be well-coordinated among governmental units. This is especially when jurisdictions related to plantation and environment sit within different government entities or territories. In Malaysia, there is a need to harmonise environmental policies for the plantation and commodities sector under Ministry of Plantation Industries with other related environmental and land use policies under the purview of other Ministries.

For instance, protecting biodiversity requires the identification and demarcation of high value conservation (HCV) areas and collaboration between Federal Ministries and State Governments, as custodians of land matters, to put in place sustainable management plans. This may include working towards certification, or an outright halt to new plantations which may encroach into HCV areas through plantation licensing enforcement. Plantations and HCV areas can coexist and balance socioeconomic needs of rural areas and ecological preservation.

Making productivity more competitive

Higher yield necessarily means reduced land use but unfortunately, it is on a declining trend. In Malaysia, the national FFB yield has declined from 19 tonnes/ha in 2012 to 18 tonnes/ha in 2017.[8] The declining productivity was primarily due to labour shortages, slow replanting of old palms and therefore, slower regeneration of palms with higher-yielding planting materials. There is a need for faster replanting to create a new generation of oil palm areas that have higher yields and are more labour-friendly, leading to improved productivity.

Another key strategy is to accelerate the discovery of even more superior oil palm seedlings. Existing conventional breeding methods of cross-breeding and hybrid take a long time to show results, as it goes through a breeding cycle of about 10-12 years. The advent of genome editing (GE) can fast-track the new development of planting materials, cutting the long development duration and delivering better results. Desirable traits such as lower palm height, shorter fronds, longer fruit stalks, low-shedding fruits and disease resistance can become a reality significantly faster with the deployment of GE.

Labour productivity has increased in recent years in Malaysia due to increasing mechanisation. Productivity increased from 0.68 tons/day per worker to 0.88 between 2012 and 2017. Yet, more can be achieved through a combination of brownfield and greenfield approaches. The brownfield approach seeks to adapt, prototype and deploy existing mature applications from other crops or regions across the upstream value-chain. The greenfield approach, on the other hand, encompasses an end-to-end new system of production with deployment of digitisation, Internet of Things (IoT) and big data analytics. This is a long-term process requiring innovation and it is critical to get started right away.

Fuelling energy needs

Palm oil is a well-established source of green fuels and chemicals. The crop can do more in this role.

Despite efforts to eventually phase out fossil fuels from the transport sector, fossil fuels are here to stay for the foreseeable future. Therefore, there is still some room for growth for palm biodiesel. In Indonesia, domestic blending has been mandated at 20%, moving to 30% by 2019, while in Malaysia, renewed efforts certainly can be made to increase the current blending from seven% to 10% for both transport and industrial sectors.[9][10]Elsewhere, commitments to the Paris Agreement by China and India to reduce their Greenhouse Gas (GHG) emissions per unit of GDP by 33% and 60%, respectively, by 2030 present an opportunity for biodiesel blending in both countries to decrease their GHG emission.[11]

Be that as it may, the future of palm biofuel is in advanced biofuel. It is a complete substitute for conventional fuel – fully compatible, mixable and interchangeable – without requiring any adaptation of the engine or infrastructure that can support all transportation modes, including aviation. This development will involve a longer gestation and significant investment, but it is a pursuit that must be made.

On the other hand, the global oleochemical market size is projected to hit USD30 billion by 2024 while the global nutraceutical market size is expected to be USD285 billion in value by 2021.[12][13]The industry is moving higher up the value-chain by producing derivatives and phytonutrients used in major consumer and health-based products that will unlock more value from palm oil.

The golden crop is here to stay

The beauty of palm oil is in its versatility and efficiency. Not only is palm oil a stable and healthy source of edible oils and fats, it also infiltrates every aspect of human life, encompassing foods, consumer and household products, fuels and lubricants.

As a global market leader, headwinds are only to be expected. The good news is palm can be even more efficient and sustainable, and that may just be enough for it to stay competitive for the long run. Wither, it will not.

[1] Source: United Nations Department of Economic and Social Affairs (UN-DESA)

[2] Source: Envisioning Malaysia 2050: A Foresight Narrative, Akademi Sains Malaysia

[6] Source: Ministry of Primary Industries, Malaysia

[7]Teresa Kok: Govt to stop oil palm expansion, keep 50pc land as forest | Malay Mail. (2018). Malaymail.com. Retrieved 5 September 2018, from https://www.malaymail.com/s/1669208/teresa-kok-govt-to-stop-oil-palm-expansion-keep-50pc-land-as-forest

Mining and quarrying have been age-old practices in Oman dating back more than 2000 years. The Sultanate is endowed with a variety of mineral deposits such as chromite, gypsum, limestone, building materials and marble. These minerals remain an important asset to Oman’s economy, with the country still possessing approximately 97% unexploited mineral potential from its industrial and metalliferous deposits.

While the mining sector acts as a catalyst for the growth of core industries like steel and cement, its contribution to GDP is still very modest at 0.5% as of 2017. One reason for this is because the sector is led primarily by small-to-medium sized companies, dealing mostly in traditional mining industries such as building aggregates. Given the low-value, high-volume nature of these industrial minerals, there is limited potential for increasing contribution to the overall Omani economy in its current form. The past 5 years have seen production value drop by 3.4%, even though production volumes have grown by 4%. The complex nature of regulating the mining industry has further compounded this scenario. Impediments to investment and growth include the lack of an attractive investment environment and inconsistent enforcement of regulations, particularly in the collection of royalties, and tedious licensing processes. This highly capital-intensive industry also demands a consistently updated geological data at national level, which Oman does not yet possess.

Given the combination of these factors, existing investors and mining operators are limited in number and the country has seen a noticeable reduction in exploration and developmental projects. This impacts the sector’s growth and sustainability prospects and its potential contribution to GDP.

Against this backdrop, Oman recognised that significant steps are required to remove the obstacles to sector growth. To lead the sector’s transformation effort, the Public Authority for Mining adopted a collaborative, result-driven approach for Oman with the introduction of the Mining Lab via PEMANDU Associates’ Big Fast Results Lab Methodology. The lab focused on three key pillars: optimising industrial minerals value contribution, reviving significant value contribution from metalliferous minerals and improving the sector’s business environment and governance.

Investors and Private Sector lead the way

When attempting to identify the real economic potential of these industrial minerals, many conclude that a simple extract-and-sell strategy is sufficient to generate growth. The Lab provided a platform of discourse and rigorous analysis which revealed that this widely held view was untrue. Despite the availability of these natural resources, Oman struggled to deliver a competitively priced product to market. The final cost of industrial minerals such as limestone are highly dependent on the geographical distance and logistical requirements between both the source mines and the destinations seeking the commodity. It was therefore important for Oman to find ways to capitalise on its geographic location to reduce the cost-to-market.

Source: Oman Mining Lab

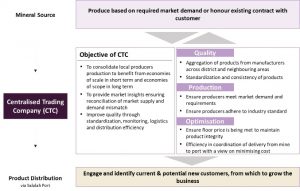

Following careful consideration and selection, the Lab recommended the formation of a Centralised Trading Company (CTC) led by a consortium of private industry players to optimise the handling of outgoing production to better fit market demand. The CTC will look to maximise value extraction by also optimising available logistics and exhibiting strict cost discipline to derive maximum value for the country’s producers.

To complement the CTC, focus will also need to be shifted beyond upstream activities towards higher value downstream manufacturing. The Lab identified and prioritised nine private sector-led integrated downstream industrial minerals projects aimed at delivering tangible results leading up to 2023. Amongst the pathfinder projects include the extraction of basalt to produce continuous basalt fibre, the extraction of dolomite to produce magnesium metal and the extraction of potash to produce premium grade potassium.

Despite metalliferous minerals being the high value contributor amongst the existing commodities, new exploration activities have dwindled over the past decade with almost no new development projects to replace ageing mines. This is particularly evident in the copper sector where there are currently no active mines despite strong proven resources available in the country.

The Lab nevertheless enabled the identification of private sector-led upstream and downstream projects for copper and chromite, along with potential downstream development opportunities in magnesium and silicon. These projects include 14 copper project sites and three new concentrator plants to reinitiate copper production and enable feed to downstream by import substitution of concentrates.

Aside from copper, 28 private investment -led chromite project sites and one beneficiation plant were identified to increase chromite production and optimise utilisation of local chrome resources in Oman, which can be fed to downstream ferrochrome plants.

After six weeks of robust deliberations, the Lab successfully unlocked the Washihi Integrated Copper Mining Project, Oman’s first copper mining project in 14 years. The project marks a resumption of copper mining activity, which truly is an example of Big Fast Results in action.

It’s all about the right Business Environment

With investors ready to commit, it is imperative that the business environment is made as conducive as possible to realise these investments. The existing licensing process requires dealings with eight different government entities whilst there is little transparency on the tax and royalty regime – these will now need to change.

Firstly, it was decided that the licensing process will be simplified via a single entity adhering to a clearly stipulated approval timeline and implementing a pre-approval clearance mechanism. With the introduction of this new process, previously lengthy license processing timelines that could take months and sometimes years will now be a thing of the past. This will also eliminate the prior lack of standard operating procedures that necessitated investors to follow-up with the Public Authority on the status of the requested approvals regularly on their own.

Secondly, the Lab also recommended a dynamic royalty rate to replace the previous flat royalty rate of 10% across commodities; a rate which is relatively higher than in other mining countries. The proposed dynamic royalty initiative will apply commodity-based formulas where different minerals will be subjected to different valuation methods or rates. In addition to this, the Lab also proposed a royalty discount mechanism upon fulfilment of certain set criteria which include downstream production promotions, amongst others. Such incentives should ensure higher in-country value and will incentivise industry growth.

Exciting times now lie ahead for Oman’s Mining sector and there is great optimism on the newly-formed winning coalition between the public and private sector. Oman has taken bold decisions and significant steps towards improving the outlook for the sector. In total, the Labs unlocked more than 10 new exploration licenses and documented another 50 applications to be further reviewed for potential approval. This injection of urgency is a far cry from the original state of having minimal to no new exploration projects.

With committed private investments amounting to more than OMR50 million for shovel-ready projects, the Public Authority of Mining is committed and fully aware of the need to lead the way in breaking down the silo mentality that often permeates within Government. All that remains is for the key industry and Government stakeholders to maintain the discipline of action and stay the course that they have plotted together. The mining engine of Oman has gotten a much-needed restart and the country hopes it will begin to truly fulfill its untapped potential.

The word ‘govern’ comes from the Latin term ‘gubernare’, which means ‘to steer’. However, the success of any government has less to do with the act or omission of steering, but more to do with ‘what’ and ‘how’ it has steered.

Our experience around the world has shown that many governments inherently have several challenges in discharging their responsibilities. Chief among them is the lack of clear focus on their strategic priorities, as most governments are unable to resist the temptation to do more in every area. Even when they get their priorities right, governments are large entities and tend to work rigidly and in silos, without detailed, implementable programmes.

Successful governments invariably exhibit both ruthless focus in areas where they can or work to be competitive, as well as having a practical execution plan that they facilitate, with recursive iterations in implementation.

Ruthless prioritisation

Ruthless prioritisation is totally necessary given that resources such as time, man-power and funds are always finite. Governments must prioritise sectors and industries that would create the most beneficial impact for its economy. This would enable the government to dedicate the right amount of resources to ensure that these prioritised areas can be facilitated for increased growth. It also acts as a signpost for investors to know what areas their investment will be given the whole of government support and facilitation.

Singapore, with no natural resources, set its mind very early on to focus on services supported by evolving manufacturing activities. Today, it is one of the world’s leading financial and logistic hubs as well as high-value R&D and industrial centres. In a similar vein, South Korea prioritised on export-led industrialisation as their main strategic plank, focusing on heavy industries and ICT activities.

Following the global financial crisis in 2009 and with an economy stuck in the middle-income trap, Malaysia too decided to embark on a more pronounced productive sector prioritisation. Blessed with natural resources to produce agriculture and fossil commodities, rapid downstream value-addition to these sectors was pursued to secure markedly higher income.

For instance, the oil and gas sector developed its erstwhile neglected mid and downstream value chain more concertedly, investing in storage and integrated petrochemical complexes that also allow it to tap higher value market segments but also paved the path into trading activities. Meanwhile, palm oil diversified very rigorously from edible oils and fats and basic oleochemicals to much richer segments of oleo derivatives, nutraceuticals and pharmaceuticals.

With a solid base in the electrical and electronics industry, steps were also taken to move up the value chain while closing the gaps in components, devices and services value chains along the way. Efforts were focused on three catalytic sub-sectors namely, electrical and electronics, chemicals, and machinery and equipment (M&E), with aerospace and medical devices identified as adjacent sub-sectors with high-growth potential as part of a 3+2 strategy. (Note: 3+2 refers to segments in E&E, chemicals and M&E plus aerospace and medical devices.)

Malaysia is fortunate that its earlier industrialisation path, driven primarily by FDIs in assembly of E&E & M&E products, created a complex economy that made later industrial prioritisation under the National Transformation Programme, including expansion into areas such as Internet of Things (IoT), aerospace, advanced materials and medical devices, an easier task.

It literally took a leaf from Ricardo Hausman’s theory of monkeys and trees[1]. The renowned economist uses the metaphor of a forest, where products are trees and firms and talent are monkeys. The closer the trees are to each other, the easier it is for monkeys to swing from tree to tree. “Economic development,” he said, “is the process of the monkeys colonising the forest.” In the Malaysian context, sub-segments such as E&E are the trees. They are heavily populated and primarily located in the northern corridor. They also produced highly skilled talents that have been able to spread into adjacent sub-sectors such as aerospace and medical devices due to common skills such as precision engineering and robotics.

Active Facilitation

Strategic direction for economic development alone is not sufficient. It needs to be complemented by active facilitation during the delivery and implementation of strategic economic plans and projects. This entails building the collaboration between the public and private sectors to improve cohesion and obtain results from these projects. Once key economic areas have been identified, the implementation of priority sector projects identified need to be closely monitored and where necessary, intervention and problem-solving needs to be carried out to resolve any implementation issues.

Having a multi-layered governance structure that operates both intra-ministry as well as inter-ministry is crucial. A multi-layered governance would improve communications between and within ministries to ensure programmes are implemented and problem-solved with the support of all relevant stakeholders. Governance will be even more effective if it has the commitment of the highest leadership, who can act as the ultimate arbitrator, especially on cross-ministry issues that hold back project implementation.

Invest KL, a special purpose unit set up in 2011 with the sole objective of attracting 100 MNCs to set up regional hubs in Greater Kuala Lumpur, is a good example of successful active facilitation. It proactively scouts and handholds the investors’ entire investment process, in collaboration with other counterparts in the government such as the Malaysian Investment Development Authority (MIDA), the Kuala Lumpur City Hall and Ministry of International Trade and Industry (MITI). As at end-2017, Invest KL has attracted 73 MNCs with investment commitment of over RM11 billion and almost 11,000 jobs created[2].

Similar successes were recorded across the prioritised sectors, from resource-based industries to services sector, thanks to the robust and effective governance structure that was put in place.

Delivery Units Deliver

First established in the UK as the Prime Minister’s Delivery Unit (PMDU) in 2001, the delivery unit model was emulated in Malaysia (PEMANDU – Performance Management and Delivery Unit) as well as Chile, Albania, Romania and Indonesia under different monikers at the national level. Conceptually, it is a discrete unit at the centre of government with a mandate to improve citizen and economic outcomes and improve oversight on government effectiveness and efficiency[3].

In engaging key stakeholders to establish priorities, delivery units provide clarity to investors, both foreign and domestic, on sectors that will receive support in terms of resources and attention. This greatly helps them in making their final investment decisions. In addition, by proactively facilitating the implementation process, the investment hits the ground much faster, which also translates into earlier return on their investment.

The delivery unit model shares many features of the Problem-Driven Iterative Adaptation (PDIA) approach which hinges on trying, learning, iterating and adapting[4]. It promotes active experiential and experimental learning with evidence-driven feedback built into regular management that allows for real-time adaptation.

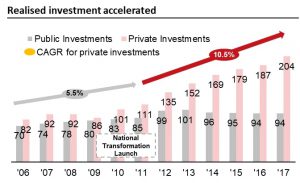

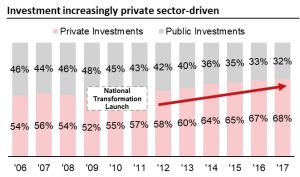

In the case of Malaysia, the economy flourished and investment gushed in with the introduction of the National Transformation Programme that was launched in 2010 and overseen by PEMANDU. The growth rate of realised investments almost doubled following the establishment of the delivery unit. Additionally, the share of private investment increased to 68% in 2017 compared to 52% in 2009 prior to the formation of the delivery unit.

Department of Statistics, MalaysiaSource: Department of Statistics, Malaysia

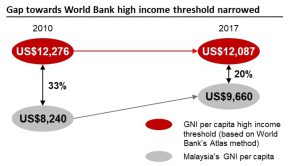

The investment levels achieved contributed to Malaysia’s growth with GDP consistently in the range of 4% to 6% since 2009, and the gap towards the World Bank’s high income threshold in terms of GNI narrowed from 33% in 2010 to 20% in 2017. Malaysia ranked 24th in World Bank’s Doing Business Report (2018), retaining its spot among the world’s top 25 economies on the Doing Business measures.

Source: World Bank

While the outcomes of the delivery unit model vary from country to country, and even from area to area, it undoubtedly assists governments in prioritising the ‘whats’ and further improving the effectiveness of processes to get things done.

From the case of Malaysia, the answer to the rhetorical headline question is firmly in the affirmative.

PEMANDU Associates’ Learning AcademyMasterclass returns with a one-day workshop focused on improving participants’ ability to structure their communication as well as develop and deliver compelling and impactful presentations in their engagement with their superiors. This workshop is targeted at young executives to mid-management executives.

Agriculture quality standards have become imperative not only to ensure safe and quality products but also for farmers to access international markets.

A highlighted by the World Trade Organisation (WTO) and academicians, tariff barriers have been replaced by sustainable requirements for market access as a means of protecting domestic producers. Understanding the requirements of the importing country and ensuring these elements are incorporated and harmonised with the standards of the importing countries is key as defined by the WTO Technical Barriers to Trade, an agreement which strongly encourages members to base their measures on international standards as a means to facilitate trade. Hence, it is essential for Malaysian farmers to practice Good Agriculture Practices that are aligned with international standards to access these markets.

These standards were introduced in accordance with Malaysian Standards that define processes in resource management for good and sustainable agriculture production which improve farm productivity and ensure produce is safe and of quality, with the welfare and safety of workers taken into account.

Spearheading a new approach to standards adoption

However, the introduction of the local standards brought on a different set of challenges. Among those highlighted by the farmers were limited market access, insufficient capacity building programmes to assist in compliance to standards, as well as questions from the importing countries on the standards applied. The value of certification was also questioned by farmers who saw the exercise as adding more work to an already laborious industry. Consequently, farmers were selling to middle-men, often at a minimal price, who were able to stretch their own profit margins through with their ability to penetrate the hypermarkets and as well as the export market.

To overcome these challenges, a mini-lab facilitated by PEMANDU Associates (during its time as a Delivery Unit in the Prime Minister’s Department) in collaboration with the Ministry of Agriculture was held, involving farmers associations and other relevant agencies. It was decided in the mini-lab that a rebranding of all three schemes under a single brand name was to be introduced to create a brand name that is easily recognised in the foreign market – this standard would also be harmonised with all other good agricultural practices used by other countries for the export market.

Thus, a series of focus group meetings chaired by the Undersecretary of the MOA as well sessions with the then-Minister of Agriculture, led to the birth of the Malaysian Good Agricultural Practices (myGAP) in 28 August 2013. Since then, myGAP has become known internationally and is synonymous with other standards such as GlobalGAP, JGAP (Japanese certification) and China GAP (China certification), to name a few.

Further to this, the MOA and its respective agencies also stepped up efforts in educating the public on the importance of certification to ensure sustainability, quality and lastly to also allow for market access, with the respective departments aggressively involved in promoting myGAP in their bilateral talks for market access. All main initiatives and sub-initiatives had individuals accountable for its implementation who were able to provide regular and comprehensive progress reporting.

Breathing new life into Malaysian produce

After the launch of the myGAP Certification and its brand promise of “Producing More, Improving Lives”, the MOA continued to work with various stakeholders to not only educate the farmers about the need and benefits of myGAP, but also encourage them to look beyond just farming but towards creating a safe and sustainable community. In an effort to further enhance the standards usage among farmers, MOA also allocated funds to assist farmers in upgrading their storage, sewage, collection, and other facilities that are requirements under the myGAP certification programme. Besides funding assistance, farmers also benefited from capacity-building programmes, awareness and promotion programmes.

The capacity-building programmes involved educating the farmers on the requirements of myGAP and its importance, which was then followed by assistance in completing the checklist in preparation for compliance and audit. This effort encouraged strong participation from farmers who were keen to understand the certification process.

Mr. M. Kaliyannan, who puts his customers at the top of his priority, has adopted myGAP in his 39-hectare watermelon farm to ensure higher standards of quality and safety for his crops. With myGAP, he has been able to widen his market for Grade A watermelons to foreign markets such as Dubai and Hong Kong. His revenue has increased more than 20% when compared to before myGAP.

“Under myGAP, there are many practical steps to follow including staff training, usage of pesticides, safety, and best practices for planters. I’ve seen many positive results since the adoption of myGAP.

“My ambition is to be the king of watermelon in Malaysia by exporting my entire Grade A products to the rest of the world. The myGAP programme is a good initiative, especially to assist us in the agriculture sector shared. I would definitely continue to encourage other farmers to follow my steps so that they can be successful as well,” he says.

Beyond addressing the supply side, the MOA also worked with hypermarkets in running awareness campaigns and promoting certified produce to encourage consumers to demand for produce that are certified. This has resulted in benefits for farmers by leveraging hypermarkets as a means of directly accessing the customer and avoiding the middle-man, and MOA’s efforts in increasing the number of certified farms in Malaysia.

Giving farmers a leg up into foreign markets

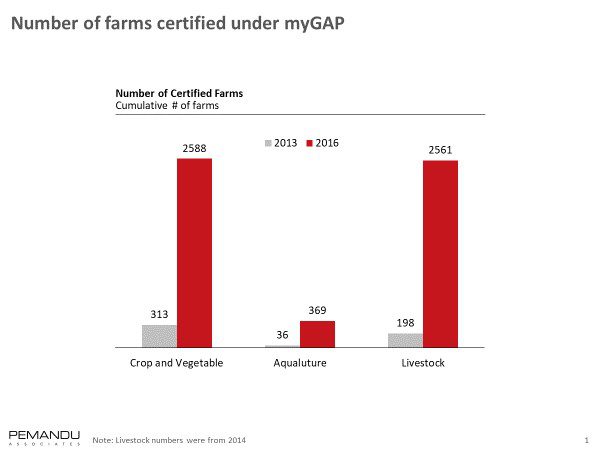

In 2017, with the introduction of myGAP, the cumulative number of farms certified with myGAP increased by 451% from 1,378 farms in 2011 to 6,226 farms in 2017, as more countries require the certification for the export of fruits and vegetables. Brunei become the most recent adopter of the certification, starting in January 2018. There was also an increase in the number of livestock farms were certified by the Department of Veterinary Services, as China, a major market for edible birds’ nest, started making it mandatory for bird’s nest imports from swiftlet farms to be myGAP certified, further proving that adopting international standards does help secure local exporters’ market penetration.

To further strengthen the transition to a globally accepted standard, the Ministry included routinely monitored KPIs that trigger problem-solving sessions which allow for effective intervention. The result of the effort is felt by the operators, as demonstrated by the following feedback received in a survey commissioned by Standards Malaysia back in 2014:

Farmers acknowledged that myGAP propagates prudent and economical administration of chemical fertilisers, which in turn helps check/control pest infestation, contributing to increased yield and reducing cost.

The feedback obtained from the farming community shows that while the process of converting from a local to a global standard does come with a learning curve and temporary pain points, the benefit of securing market access and improving profits is well worth the investment. The transformation to the global standard was made possible by bringing the public and the private sector together to problem-solve anticipated issues for the conversion, and relentlessly monitoring the work toward a common purpose.

“Before I adopted myGAP, I had to spend about RM16,000 on chemical fertilizers, but after the adoption, I was able to save money because I only spent RM2.000 by using the Sri Product via the Natural Farming concept. Now, I am using 70% of Sri Products and 30% chemical fertilisers. With myGAP, I am able to sell my rice for RM6.00/kg compared to before when it was only RM2.00. I have also sold rice seeds to Sendi Enterprise for RM1,350/tonne and sold rice at RM1,200/tonne to Bernas.” – Abdul Razak Chik, better known as ‘Pak Lang Sri’, who owns a paddy farm in Sekinchan, Selangor.

The gas industry is a substantial component of Oman’s economy, contributing significantly to export earnings and serving as an important enabler to local industries. In 2017, Oman produced 41 billion cubic feet of gas, of which 32% was exported by Oman LNG while the remaining 68% was consumed locally, with consumption growing at an average of 2.3% per annum for the past eight years. Its proven total gas reserves stood at 25 trillion cubic feet as of end-2017.

As a GCC country rich in natural resources, Oman’s gas reserves are however a finite asset. Its current supplies remain healthy in the short-to-medium-term, but with pressure now to diversify the economy and reduce its over-reliance on oil and gas, its gas assets will need be utilised to directly spur other economic sectors. Gas requirements for economic generation, particularly in the manufacturing sector, will need a long-term supply commitment, and the country will need to balance this with its existing industrial and residential commitments, the latter of which continues to grow as the nation’s population increases.

Against this backdrop, and as part of a wider programme of economic diversification, the Omani Government saw a need to carefully manage supply and demand in the gas industry to mitigate any probability of a gas deficit situation in the medium-term. The supply-demand dynamics were further impacted by the fact that 97% of its power was generated from gas-fired plants. From an energy security perspective, Oman needed to consider diversifying its sources and avoid over-reliance on gas. Preserving this precious finite resource and allocating it to industries that generate the highest economic returns then became a priority for long-term sustainable development.

Complementing the effort to manage its gas resource was the need for effective governance that provided a conducive planning and regulatory environment for Oman’s industry players. The Ministry of Oil and Gas serves as an able custodian for the Oil & Gas industry, while the Electricity sector is managed by separate Authorities who do their best within their respective mandates. Moving forward, consolidation of the strategy and planning of these two closely related sectors would allow for harmonised development, taking into consideration a rapidly changing economic landscape.

Delivering tangible transformative outcomes

Through the PEMANDU Associates’ BFR Methodology Labs, Oman devised and adopted a 3-pronged strategy specifically for the Gas sector: (i) Ensuring long-term gas supply security, (ii) Optimising growth-driven gas demand and (iii) improving infrastructure capacity and efficiency.

Firstly, thorough investigation was conducted on all existing gas producing assets and development plans for greenfield projects. Specific supply-based projects were identified with the potential to increase Oman’s gas production substantially by 2042, and as a result, extend Oman’s available gas supplies. These projects include immediately implementable initiatives such as flare gas reduction, replacement of gas usage in existing operations to generate thermal energy, increasing asset productivity through modern technology; and longer-term greenfield and brownfield gas development projects.

Secondly, to complement the effort to increase gas production, the Lab deliberated on ways to optimise demand. After careful selection, a set of robust and stringent gas allocation criteria was developed and proposed. The ultimate objective was for Oman to allocate gas to industries that generate the most economic returns. Future applications for gas usage will be assessed and then prioritised using these new criteria. This represents a paradigm shift to a more objective, measurable and impactful allocation practice. In addition, a standardised gas application process was designed and communicated to all impacted stakeholders from both the public and private sector.

The third strategy for the Gas sector is to improve gas infrastructure capacity and efficiency. The Lab assessed high industrial growth areas against the availability of pipelines to meet future demand. This culminated in new pipeline projects that will transmit extra gas transmission capacity to critical regions like Sohar, Duqm, Sur and Salalah by 2019.

One of the key components in Oman’s Energy sector is the Electricity sub-sector. A comprehensive transformation of gas consumption would not be complete without assessing this sub-sector, where gas contributes 97% to all power generation capacity. There is thus a critical need for energy diversification for electricity generation to include renewable energy sources.

Two major outcomes were achieved in the Lab. First, 17 non-gas power generation projects were identified and prioritized for implementation. These projects will cumulatively provide up to 11% non-gas source generation by 2023. This is a substantial achievement considering Oman is still a developing nation with overall projected electricity demand expected to increase further in the next five years. The projects encompass utility-scale solar PV plants, wind farms and waste-to-energy plants. The Ibri 500MW solar power plant is an example of Oman’s government drive to diversify its energy source mix. This project is expected to be completed by 2021 and will be the first large scale solar project in the Sultanate.

Lastly, the Lab recommended that harmonised planning and development of Oman’s Energy Policy be institutionalised. Currently there is no one single entity, nor there exists a process that will enable the holistic development of an Energy Policy that considers interest of all sectors. The solution adopted will involve expanding the jurisdiction of a single existing entity to include policy-making for both the electricity and gas sub-sectors holistically.

Momentum for the future

The key lessons revealed through Oman’s Energy Lab is the need for a coordinated and structured approach for planning in this critical sector. Since the sub-sectors are all intricately linked, changes in policy and executive decisions must be done taking into consideration ramifications to all stakeholders. The Lab discovered that one of the biggest hindrances that industry players faced was due to the lack of central coordination of policy decisions and follow-up actions. If possible, policy-making should be centralised to encourage greater efficiency.

In addition, for a country facing diminishing reserves of a finite resource, demand planning such as consumption optimisation and subsidy rationalisation should take precedence. The political will to shift from a way of potentially wasteful cheap resource consumption to a more conservative approach of utilisation needs to be present. The BFR Methodology Labs have certainly provided the platform for a collective realisation that continued reliance on gas as Oman’s sole energy source will not be sustainable for the long-term, and has generated the momentum for the country to aggressively diversify into renewable energy. The future of energy diversification and security looks to be on the right track.

PEMANDU Associates’ Learning Academy is organising a one-day workshop focused on improving participants’ ability to structure their communication as well as develop and deliver compelling and impactful presentations in their engagement with their superiors. This workshop is targeted at young executives to mid-management executives.

Date: Monday, 30 July 2018

Time: 9.00 am – 4.00 pm

Location: Sunway Putra Hotel

Event Fee: RM750 per person

This workshop will cover:

Module 1: Structuring Your Thought Process

Module 2: Creating Compelling Presentation Decks

Module 3: Delivering an Impactful Presentation

Masterclass Introductory Bonus: Power Lunch Talk with Dato’ Sri Idris Jala, CEO of PEMANDU Associates

“The ERGP had determined US$195.98 billion in private investments required to achieve its target of unlocking sustained inclusive diversified growth for the maximum welfare of Nigerians”

The second largest economy in Africa after South Africa, Nigeria is a uniquely diverse country comprising 371 ethnic groups with over 520 spoken languages. Its economy, however, was dependent on revenues from oil exports and thus had been adversely impacted by the decline in global oil prices in 2014 to 2016.

This resulted in the country experiencing a recession in 2016, leading the government to formulate the Economic Recovery and Growth Programme (ERGP) 2017-2020 to transform the economy. The ERGP requires US$245.13 billion to implement and had determined US$195.98 billion in private investments required to achieve its target of unlocking sustained inclusive diversified growth for the maximum welfare of Nigerians.

With this agenda in hand, the Nigeria’s Ministry of Budget and National Planning, tasked with overseeing the ERGP, appointed PEMANDU Associates to synthesise its plan into realistic implementable initiatives, looking to our experience in deploying our proprietary BFR methodology in effecting economic transformation in countries such as Malaysia, Oman, South Africa and India.

Specifically, they sought help in mobilising private sector investments in six sectors identified as the economy’s most productive. The sectors were then clustered into three workstreams based on their relevance to each other: Manufacturing & Minerals Processing, Agriculture & Transport and Power & Gas.

“The initial interactions with the CEO and leadership of PEMANDU Associates was reassuring and gave a lot for the team to anticipate as to how the Labs would be run, and how this would constitute a key developmental experience for the country, the team members and the Lab participants. The CEO’s inspirational approach was therefore commendable.

The Labs provide extensive involvement of most stakeholders to co-create solutions rather than have the solutions developed by a small team of consultants or just involving the stakeholders for consultation only over a few hours.

Towards the end of the project, the PEMANDU Associates project team and PEMANDU Communications, that assisted with preparing for the Open Day, appeared very outcome-oriented and this was positive. The communications team indeed appeared very positive in their approach and this was commendable.”

– Folarin Alayande, Co-ordinator, ERGP Implementation Unit/Senior Special Assistant to the President (SSAP, Economic Recovery and Growth Plan (ERGP)

Overcoming challenges, bridging gaps

Challenges in crafting a three-feet plan for these clusters for Nigeria, as with most countries in the world, were multi-faceted, stemming from the polarity in expectations between the public and private sectors. Governments typically have a record of amending policies and plans, while the private sector are generally motivated by the bottom line, hence may be cautious in participating in grand government plans.

This was a specific challenge tasked by the Nigerian government to PEMANDU Associates to decrypt. Drawing from PEMANDU’s previous experiences in mobilising private investment, such as the US$444 billion in investments facilitated and identified under Malaysia’s Economic Transformation Programme and the 775 projects valued at US$96 billion identified in the Urban Development Lab in Andhra Pradesh, we found that most economies in the world are dependent on the public sector to spur investments and expenditure.

Our role in Nigeria was to develop and enable a programme that would ensure the government continuously works with the private sector to own, initiate and implement transformational projects that would yield positive multiplier outcomes for the economy.

Some of the Manufacturing & Processing Lab members during the ERGP Focus Labs

Thus, for much of the first half of 2018, the PEMANDU Associates project team was stationed in Abuja to conduct the necessary groundwork and undertake Wave 1 of the ERGP Focus Labs.

Under this project, PEMANDU Associates helped the Nigerian government identify US$22.5 billion in private investments which could be unlocked from the implementation of 164 projects, paving the way for the creation of 513,981 jobs.

This was done by encouraging the private sector to take a proactive participation in the ERGP Focus Labs. This proved to be a unique value proposition to the industry captains and with the support of the government who sent key decision-makers to the labs, it generated positive interest amongst the private sectors.

A total of 500 participants from both the public and private sectors, comprising the relevant stakeholders from the three workstreams, were brought together under one roof for six weeks.

Given the existing polarities, the exercise was expectedly met with its fair share of scepticism, with some private sector stakeholders turning up with their products with sales in mind, while some expected to garner public investments. Some, were taken by surprise at the level of involvement required of them, having been used to government-led economic initiatives. So, the challenge was to shift expectations and mindsets from ‘What is in it for me’ to ‘How can I contribute in terms of planning for my sector’.

Nonetheless, the presence of public sector decision-makers in the Labs, and the participants’ determination to achieve tangible results allowed them to put aside their cynicism and work towards to common goal. The private sector became the engine of the labs and the shift in conversation was a remarkable breakthrough.

“We would like to especially commend the management and project team of PEMANDU Associates for organising and facilitating the smooth conduct of the ERGP Focus Labs of the Federal Government of Nigeria, particularly the Agriculture/Transportation Projects.

Our company, Trucks Transit Parks Ltd, benefitted immensely from the programme in the following ways:

– highlighting to the government the social necessity that the project seeks to address;

– bringing to the notice of the government challenges faced by our company in progressing the project;

– assisting us to more properly package our project for fast-tracking by the government;

– enabling us identify certain inherent challenges to attracting investments into the project; and

– putting us in direct liaison with key regulators.

This would not have been possible if not for the professional approach of PEMANDU Associates’ hard-working team.”

– Jama Onwubuariri, Director, Trucks Transit Parks Limited, ERGP Focus Lab member

Getting to work

Once participants were on board, the next challenge was identifying and prioritising initiatives. Projects were categorised to their level of readiness and conversations were created to discuss their business model; from how to grow, plan and finance, with each project put under scrutiny.

These buckets of conversation separated projects ready for implementation and acceleration from projects under incubation. Creating relevant conversations which engaged participants successfully retained participants throughout the whole six weeks of the Labs, producing frank, transparent conversations.

The outcome of the Labs and its in-depth, implementable programmes were presented during an Open Day in Abuja in May 2018.

The Open Day, which was attended by the public and private stakeholders as well as the media, served to communicate the ERGP Focus Labs initiatives to the public.

Together with the Labs, the exercise served to inject greater transparency into the government’s initiatives, representing a good start for the Nigerian government to win over the hearts and minds of the country’s people in its bid to transform the economy.

In applying our 8-step Big Fast Results (BFR) Methodology, the approach in its start will always be met with a degree of cynicism. As experienced in previous projects, however, these sceptics are very quickly won over when they witness how the methodology works, our flexibility to adapt to client needs, all the while staying focused on meeting a clear set of deliverables.

Key to success in any of our BFR consulting projects has always been the team’s commitment to understand the country’s dynamics, the unique relationship between the private and public sectors, its tipping point, diversity and issues. The BFR Methodology has always allowed PEMANDU Associates to take a collaborative approach with participants to steer the conversation towards a true outcome guided by an objective. Leadership commitment and participation is always a mainstay in allowing incredible sharing of knowledge resulting in implementable outcomes.

Nigeria has today completed Steps 2 (Lab) and 3 (Open Day) of 8 and now has a clear plan for the first phase of its ERGP. The Government will now need to set these action plans into a detailed programme by way of a Roadmap for implementation. Coupled with the discipline of action and rigorous monitoring, the Nigerian Government has set itself on the path of transformation. And while the public and private sectors have painstakingly converged to realise this programme of change, the ultimate stakeholders who stand to benefit from this work are the people of Nigeria.

With a solid base in the electrical and electronics industry, steps were also taken to move up the value chain while closing the gaps in components, devices and services value chains along the way. Efforts were focused on three catalytic sub-sectors namely, electrical and electronics, chemicals, and machinery and equipment (M&E), with aerospace and medical devices identified as adjacent sub-sectors with high-growth potential as part of a 3+2 strategy. (Note: 3+2 refers to segments in E&E, chemicals and M&E plus aerospace and medical devices.)

With a solid base in the electrical and electronics industry, steps were also taken to move up the value chain while closing the gaps in components, devices and services value chains along the way. Efforts were focused on three catalytic sub-sectors namely, electrical and electronics, chemicals, and machinery and equipment (M&E), with aerospace and medical devices identified as adjacent sub-sectors with high-growth potential as part of a 3+2 strategy. (Note: 3+2 refers to segments in E&E, chemicals and M&E plus aerospace and medical devices.)

“The initial interactions with the CEO and leadership of PEMANDU Associates was reassuring and gave a lot for the team to anticipate as to how the Labs would be run, and how this would constitute a key developmental experience for the country, the team members and the Lab participants. The CEO’s inspirational approach was therefore commendable.

“The initial interactions with the CEO and leadership of PEMANDU Associates was reassuring and gave a lot for the team to anticipate as to how the Labs would be run, and how this would constitute a key developmental experience for the country, the team members and the Lab participants. The CEO’s inspirational approach was therefore commendable.